-------------------------------------------------------------------------------------------

Caution :

Contents of this posting mainly based on informations

sourced from publicly available documents,data collection and verification through private

sources and certain assumptions.Due to some practical difficulties I could not verify the authenticity of few informations provided

here ,hence no guarantee for its accuracy and prone to higher level of risk. But, to the best of my knowledge , the given informations are correct. Before

acting on this recommendation ,do own home work and take decision only

thereafter.

-----------------------------------------------------------------------------------------------------------

Let us start this new year with a prayer for a good 2014

.Last year SEBI play the spoilsport by the introduction of Periodic Call

Auction .This time,by god’s grace ,they realized the drawbacks of this

mechanism and already declared many relaxations which is expected to bring lot

of relief to small and mid cap investors going forward .

Pharma and IT were the out performers in2013.Since , political uncertainty is still

looming,investment in these sectors are still relevant.Among the pharma pack ,Ajanta

Pharma was the biggest gainer in last year.It out performed all biggies with a

wide margin. But if we take the top selling drugs in the

country it is hard to find any of the products by this company.Then

what is the secret of this out performance ?.I believe it is only because of

the sterling performance of its ‘Kamagra ‘ brand in overseas markets. This

brand gained a sizable market share in Male Erectile Dysfunction segment along

with the VIAGRA brand of Pfizer.Frankly

speaking I am not aware about the complexities of manufacturing this product (

Sildenafil Citrate) ,but it is a fact

that only a handful companies from the listed space making this product , even this segment is growing at a fast pace with good margin.

My search to find out another company active in this segment from mid cap space ends in a

small Chennai based company named Caplin Point Laboratories. Even though this company not specifically claiming as a

producer of this product, based on the

available information ,this is one of the largest exporter of the generic of

Sildenafil Citrate from India . Company supplying large quantity to Latin American and African Countries where product registration

is enough to sell medicines and regulatory requirements are not tough and also a preferred supplier for online drug

stores .If you

are ready to spend few hours in internet with some academic interest ,you can

easily gather enough proof for company’s supply of Sildenafil Citrate through these channels . There may

be some solid reasons for the non

disclosure of this fact by the company and I believe they will disclose it once

they get a USFDA approval for their new plant which is nearing completion.

Another interesting fact about this company is - it is a debt free company and getting money

in advance for supplying medicines from its distributors ! .Have you ever

heared about such a business model in case of a small pharma company in India ?.More than that ,company claiming that the

funding of Rs.75 crore for the new plant is coming from such advances and

internal accruals .Since there is no proof for its manufacturing of any

critical life saving medicines ,I believe

,advance payment is only because of the supply of sildenafil cytrate

which is in high demand from suppliers to online stores. Apart from this

product ,company also exporting many other products to countries like Guinea, Guatemala, Angola, Mali ..etc .Company selling such products under its own

brand name in these countries .(OTC Product Advertisement HERE ).

On the financial front

,company is growing steadily in past few years .Its top line improved from Rs.60 Cr to

Rs.122 Cr and net profit galloped from Rs.3 Cr to 14 Cr in last four years.Management

of company rewarding share holders proportionately in these years which distributed

a dividend of 25 % in latest financial year. Company is now going through a

massive capacity expansion program .As part of this ,company is in the process

of setting up a state of the art injectable plant which will cater to highly

regulated markets like USA ,

EU ..etc .It started construction in 2012 and and planning to complete it in three phases .First phase of this plant

is expected to start trial run in this month itself .This facility is mainly

for sterile injectables and prefilled syringes .There is severe shortage for

sterile injectable facilities across the world and big MNC’ pharma players are in a hunt for acquiring quality assets in this

segment.Mylan’s recent buyout of Agila division of Strides Arcolab at a whopping

valuation is an indication for the premium valuation for Sterile injectable

facilities worldwide .

Pre-filled syringes is relatively a new concept which is gaining

acceptance and potential is very high. Company claiming they have

already entered

in some agreements with Brazil based firms to distribute products from

this

facility . This may be a temporary arrangement till the company get the

permissions of USFDA and UKMHRA for this facility .Caplin point also

expanding

its existing manufacturing unit at

Puducherry by adding facilities to produce Suppositories, Soft gelatin capsule

and Penems.This is also expected to to start production in the second half of

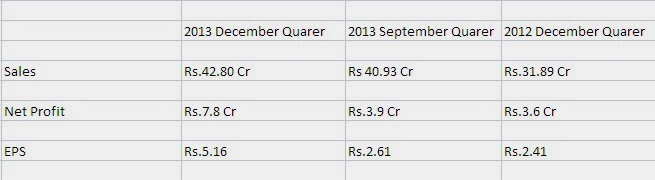

this FY. Company already recorded a sales of Rs.40 cr and a net profit of

Rs.4 Cr in the first quarter ended in September ( Company's year ends in June ) ,this figure is even after deducting a forex loss of Rs.4.6 cr.

CLICK ON THE IMAGE FOR A BETTER VIEW

Company’s balance sheet is virtually debt free and

now it expanding production capacity utilising funds at cheap cost .Company

expecting a contribution of Rs.300-400 Cr from this facility when it completely

operational.Even if the company scheduled to start operations from final phase (phase 3) of

this facility by September 2014 ,it may delay by 6 month or so.Even then

company can report respectable numbers with productions from phase 1 itself.

In pharma sector ,different companies are following different business

models.Some of them are unique in their products developed by own R&D like

Biocon..etc ,some of them are unique in production capacity which aims mass

production to reduce per unit cost ,like Granules India .In the case of Caplin

Point, uniqueness is in its well knitted marketing network across many under penetrated Latin American and African countries.Unlike many other pharma

countries which are exporting products to bulk distributors there ,Caplin point

established their own offices in these countries and selling of medicines controlled by their own offices located

there.This strategy helping the company to earn higher margins and also to get

a clear idea about the changing demand scenarios in that countries.

In nut shell let us summarise the reasoning for a positive view on

this company as below

1)

Company

is virtually debt free

2)

Promoters

accepting their faults happened in

the past and ready to change

3)

Consistently

growing in their second innings,turned to a profit of Rs.14 Cr from a loss of

Rs.2 Cr in last 5 years.

4)

No

hesitation to reward share holders ,increased dividend from 10 % to 25 % in

last four years.

5)

Well

established marketing network in Latin American and African countries with own

offices and infrastructure in these countries.

6)

Supplying

‘products in need’ ,and getting advance payment for supply ,really an interesting business model.

7)

Massive

capacity expansion without debt burden ( As per management estimates full

capacity utilisation will generate an income up to Rs.400 Cr)

8)

First

phase of new plant is ready and trail

run will start start by this month

end itself.

9)

Already

established marketing arrangements for part of the products from the new plant.

10)

Higher

promoter holding ,more than 57 % + 10.38 % held by relatives of promoters under non promoter category

11)

A

well accepted supplier of the generic version of Sildenafil citrate to many

overseas countries and online drug stores .

If the company can secure approvals from USFDA and other overseas

authorities in time,this stock will turn out as a dark horse and a re-rating

like the one happened in Ajanta Pharma is a possibility .Even if there is any

delay in approvals, it can still improve its performance with the export of

products to other countries through existing channels though the margin may be

bit lower .Even in that case one can expect reasonable appreciation from the

current level. Commissioning of its new plant will be a landmark in the history of company which will re-write the magnitude of the operations of Caplin Point .One can buy it at CMP Rs.86

Stock listed only in BSE with code 524742

Link to Company website HERE

Details of new plant HERE

Link to Annual Report HERE

Disc : It is safe to assume that I have vested interest in CPL